Cost Segregation Explained: Accelerate Depreciation & Reduce Taxes

Cost Segregation Explained: Accelerate Depreciation & Reduce Taxes

Cost Segregation: The Most Powerful Depreciation Tool Most Business Owners Never Use Correctly

If your business owns real estate, whether as an operating facility, investment property, or part of a sale-leaseback structure there is a strong likelihood you are depreciating that asset too slowly.

Cost segregation is not aggressive planning it is accurate classification under IRS rules.

The real question is not whether you qualify but how much accelerated depreciation you are leaving on the table.

The Standard Depreciation Problem

Under standard rules:

- Commercial real property is depreciated over 39 years

- Residential rental property over 27.5 years

That means a $5 million commercial building produces roughly $128,000 in annual straight-line depreciation, regardless of how quickly its interior components actually deteriorate.

But:

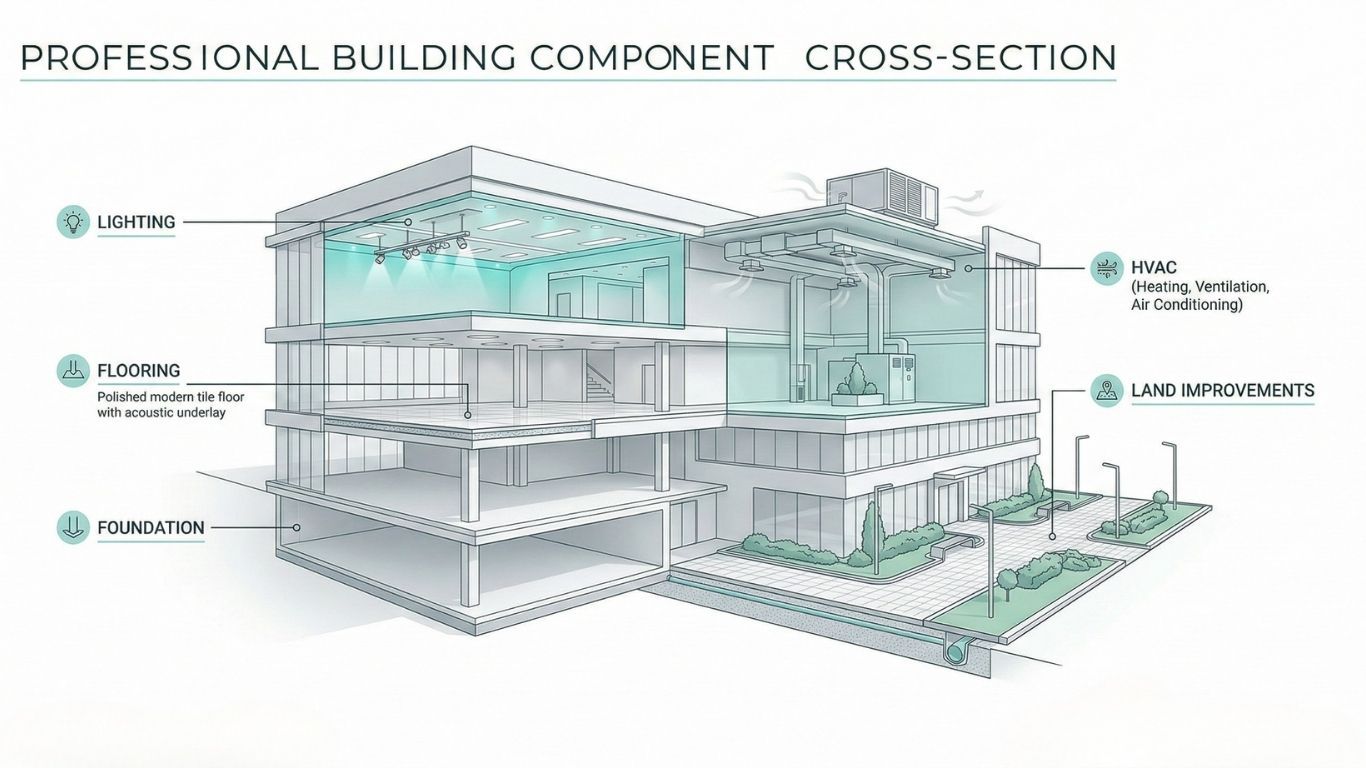

- Lighting systems don’t last 39 years

- Parking lots don’t last 39 years

- Security systems don’t last 39 years

- Specialized manufacturing flooring doesn’t last 39 years

Cost segregation identifies and reclassifies these components into:

- 5-year property

- 7-year property

- 15-year land improvements

By doing so, it accelerates depreciation into earlier years of ownership when cash flow is most valuable.

The building may last decades but many of its components do not.

Bonus Depreciation: The Multiplier Effect

Assets with a recovery period of 20 years or less qualify for bonus depreciation.

Under current law, bonus depreciation remains at 40% for tax years 2025 and 2026, before phasing down further under existing TCJA sunset provisions unless legislative changes alter the schedule.

When a cost segregation study reclassifies interior systems and improvements into 5 or 15-year property, those components become eligible for bonus depreciation.

On a $5 million commercial property, a study may identify $1.5M to $2M in reclassifiable assets.

The result?

Hundreds of thousands of dollars in accelerated deductions in year one instead of spreading those deductions across decades.

For growth-focused companies reinvesting capital into operations, this is often a cash flow accelerator disguised as an accounting decision.

Cost segregation does not create deductions it accelerates them when timing matters most.

The Sale-Leaseback Advantage

Owners who separate their real estate into a holding entity and lease it back to their operating company have already made a sophisticated structural decision.

But structure without depreciation strategy is incomplete.

A cost segregation study conducted:

- At acquisition

- At construction completion

- Or retroactively via a look-back study

can unlock deferred depreciation without amending prior returns, using an automatic change of accounting method.

This is particularly valuable for owners who purchased property years ago and never revisited their depreciation strategy.

Cost segregation is not just for new purchases it can unlock value from past decisions.

Passive Activity Rules: Who Can Actually Use the Deduction?

Accelerated depreciation often produces paper losses.

But whether those losses are usable depends on:

- Whether the property is passive or non-passive

- Whether the owner qualifies as a real estate professional under IRC §469

- Whether income grouping elections have been made

- Whether suspended losses will be released at exit

Many owners assume accelerated depreciation automatically offsets operating income.

That is not always the case.

Understanding the passive activity framework ensures depreciation strategy aligns with actual tax outcomes.

The goal is not just generating deductions.

It is generating deductions you can actually use.

Accelerated depreciation is powerful but only when integrated with your overall tax structure.

Timing Matters: When to Commission a Study

At Acquisition or Construction Completion

This is the cleanest and most efficient time.

Retroactively via Look-Back Study

Available for properties placed in service as far back as 1987 without amending prior returns.

Before a Sale

Helps maximize depreciation before disposition and evaluate recapture implications.

The cost of a quality engineering-based study on a $5M property typically ranges between $8,000 and $15,000.

The first-year tax benefit often exceeds the cost multiple times over.

This is why sophisticated real estate investors, manufacturers with owned facilities, and construction companies investing in yard properties evaluate cost segregation as part of capital strategy not just tax season.

The study cost is measurable. The missed depreciation often is not.

The Bigger Picture

Depreciation is not just an accounting entry.

It impacts:

- Cash flow

- Debt service coverage ratios

- Reinvestment capacity

- Expansion timing

- Exit value modeling

Cost segregation is not a loophole. It is the accurate application of IRS depreciation rules.

If you own commercial property and have never had a dedicated cost segregation discussion as part of your broader tax strategy, that conversation is overdue.

If you would like to evaluate whether your property portfolio is optimized especially in light of bonus depreciation phase-down schedules, we’re happy to review it.